My remarkable budgeting ways to reach the illusive Financial Independence

Before you can invest and build up your portfolio you have to start with the basics: budgeting. It’s safe to say managing your budget is a key point to reach Financial Independence.

I’ll be honest, I’ve been budgeting my finances well before I discovered FIRE. I believe it’s a sensible thing to do if you want to stay on top of your finances even if you don’t plan to retire early.

I’d recommend it to anyone. Budgeting is the first step into a whole new world. A world where you don’t have to worry about there being too much month at the end of your paycheck, not worrying about whether or not you have enough to pay for the broken freezer, or being able to pay unexpected expenses.

How I started budgeting

In the beginning, I kept track of my finances to know where my money went and if I wasn’t paying for something I wasn’t using anymore.

I originally looked into using an Excel spreadsheet to keep track of my budget, but during my search for templates, I stumbled upon YNAB AKA You Need A Budget.

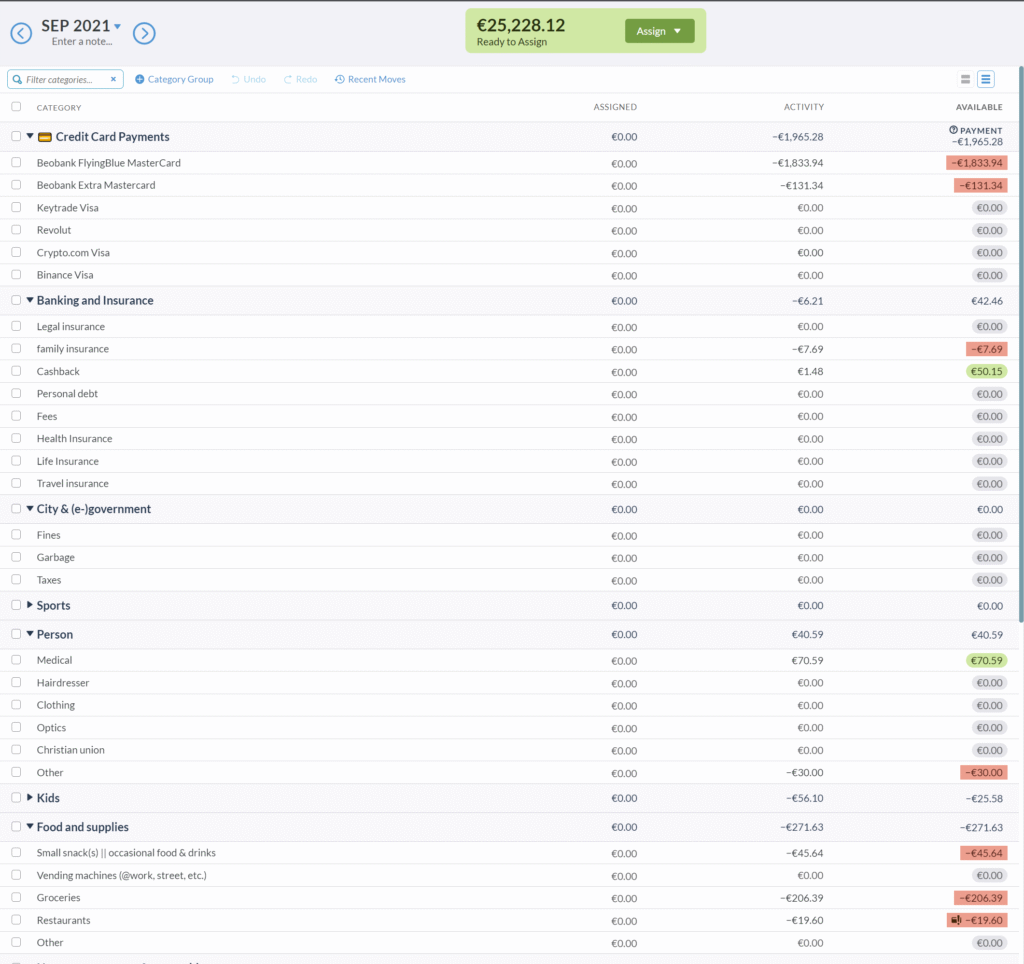

Why YNAB?

You might wonder why I bothered with YNAB and not just use Excel or Google Sheets if I don’t use the key feature of the tool.

Well, I used the trial version of YNAB for a month, not planning to take the full version. However, this changed after I used that free trial. I really enjoyed the simplicity and clean interface, also the graphs it provided were excellent. YNAB offers more than just the budgeting part to help you with your budget.

Besides, I also don‘t need the full flexibility of Excel (or Google Sheets).

My needs are straightforward and are all met with YNAB:

- A place where I can generate a nice overview of my income and expenses

- Straightforward graphs showing my spending

- In a simple overview

- My spending trends (how much I spend on what every month)

- Income vs. expense

- Net worth

Every euro already has a job

As a result of my frugal mindset I never really had a problem not throwing money down the drain.

Of course, we are talking about my teen years and early adulthood so expenses were limited. It’s not like most people in this period of their lives have major expenses anyway. That said, I did notice that some had a lot more difficulty in keeping their money in their pockets.

Interestingly enough, I read an article about this exact topic just this week. I will write a separate post later. Basically, Swedish scientists investigated the saving behavior of twins that showed that genetic predisposition is most important in the setting aside of money. The saving behavior of identical twins was similar, while that of non-identical twins could differ, despite the same upbringing. Food for thought, right?

I have a natural tendency to think about how I use each euro I have, in other words, what job I give each euro.

The downside is that I can be indecisive when it comes to purchasing goods. Even smaller things such as earbuds, a new keyboard, etc.

Budgeting towards FIRE

My indecisiveness towards purchasing things is a nice way to take us towards the future: how will I handle my budget to finally reach what most (or at least those that read this blog) hope to achieve, financial independence?

After all, the money you spend on one thing is money you can’t spend on something else. This idea even has a nice name: opportunity cost. On top of that, what you buy has an impact on your budget for future purchases.

Keeping my expenses in check also helps me reach my personally set target Savings Rate (or SR) of at least 75%. With a savings rate of ~85%, I went over it by a good margin these last 6 months.

The term “savings rate” I just threw in there is something you will have come across if you reached this site to read more on FIRE, as such I doubt I’ll have to explain what it means. Nonetheless, it will come back later when I talk more in-depth about my way of living to reach such a high SR.

Keeping up with the Savings Rate

Keeping my SR at 85% is easy now due to my current way of living (with my parents), so I know it’s not realistic to think I can keep it up once I decide to move out. As long as I’m not on my I do plan to keep it as high as possible, i.e., around 85%.

Once I’m on my own, I’ll be happy with something like 50% – 60%. The exact level will depend on how I manage of course, so only time will tell.

Update 09/01/2019: In the meantime I created a post with a guestimate of my target FIRE age.

Another YNAB geek here! I do pay for the yearly subscription of the nYNAB, however I only pay 50 dollars per year, which is around 42 euros. That’s definitely worth it to me. Also, every now and then I refer someone to YNAB, yielding both me and the new customer a free month. Not too bad!

If you every want to upgrade, let me know. I have a free month for you :-).

Keep on budgeting and killing it with your savings rate buddy!