Curve Card Review: The best Card To Rule Them All!

My Curve Debit MasterCard has been in my possession for over a month now, so I figured I’d share my experience with everyone having it used both in Belgium and abroad (in South America). Eventhough it’s only been one month, this card has been impressive. Thanks to unique features and ease of use, it’s a must-have for everyone!

Where does Curve come from?

It’s a British company founded in 2015 by Shachar Bialick, trying to simplify banking on a whole new level: Curve connects all your cards in one smart card and one smart app with an extra layer of goodness. This is only the start of their plan. Expect more to come in the future.

How to get started with the free Curve card

After I upgraded to Jade Green with Crypto.com, I decided to follow through on my own advice in the review I wrote and start using Curve. The process is straightforward and doesn’t take much time. Provide the basics KYC information, and your card is on your way right away:

- Download the Curve app

, and choose which card you want to order. A free card will give you the basics and one month of 1% cashback!

- Add all your credit and debit Visa and MasterCards in the app, so you never have to carry them physically. Don’t forget to choose a fallback option using the ‘Anti-Embarrassment Mode.’ Go to ‘Account’ -> ‘Settings’ -> ‘Anti-Embarrassment Mode’ where you can choose up to two backups.

- Use the camera to scan and upload your card details (e.g., Belgian id) automatically or enter them manually.

- Activate your physical Curve Debit MasterCard in the app once you receive it. Go to the “Account” tab and tap “Activate your card”. You’ll be asked to enter the last 4 digits of your Curve card, and that’s it.

- Choose which card you want to pay with by swiping through your digital wallet in the app and tapping the card you need. Then, you can use your Curve card like you would any other card in your wallet. Once you activate the Curve card (step 4) and add your other cards (step 2), you’re ready to pay.

- You can go card-free by hooking up your Curve card to Apple Pay, Google Pay, or Samsung Pay. Any card you add to Curve will work with them, even if your bank doesn’t.

(First) Uses

Once received, the first thing I did was leave my Visa and Mastercards at home. It was one of the main perks: pay for everything with one card.

Except one card. My crypto.com Jade Green card stayed in my cardholder. I’m abroad, and the Crypto.com card has no exchange fees when purchasing goods in a foreign currency which is exceptional; I don’t know how long they will keep that up.

Having linked my cards, I got 1% Curve cash for purchases that I had to do anyway. My spending didn’t change, but I was now getting 1% Curve cash (for 30 days) and crypto for doing groceries.

During the first 30 days of using the card, I was abroad and used the card till I reached the 200-pound exchange limit. It really served me well, because I had two occasions where my crypto.com card got refused for some reason and one time where I didn’t top it up on time.

Lots of support, but not all!

While doing step 2. when requesting the card, there are a few limitations to which cards you can add. All of your virtual or physical Visa, Mastercard, Diners Club, and Discover debit and credit cards can be added to Curve. But there is no support for American Express, Maestro, JCB, or UnionPay cards. It doesn’t matter if the card is virtual or physical.

American Express is a big one but apparently, Amex doesn’t want to hand over control of their user experience to another party.

Can you trust Curve with your card details?

Curve is registered under FCA for UK cardholders and in the aftermath of Brexit secured an eMoney licence in Lithuania, becoming an Electronic Money Institution (‘EMI’) in October 2020, with European Economic Area (‘EEA’) passporting rights secured in November 2020. On 31 December 2020, at 11 PM GMT, all EEA cardholders migrated seamlessly to their new EEA Electronic Money license. In other words, they are regulated by trusted entities in both Europe and the UK.

Moreover, the card has an aggregated review score of 3.9/5 from thousands of reviews on Trustpilot. 84% give it a ‘good’ or higher, with 13% giving a one-star score. The bad scores are in large part related to slow customer support and in minor part to declined transactions.

Combining both the regulation and overall good customer feedback makes Curve a company you can work with as a consumer.

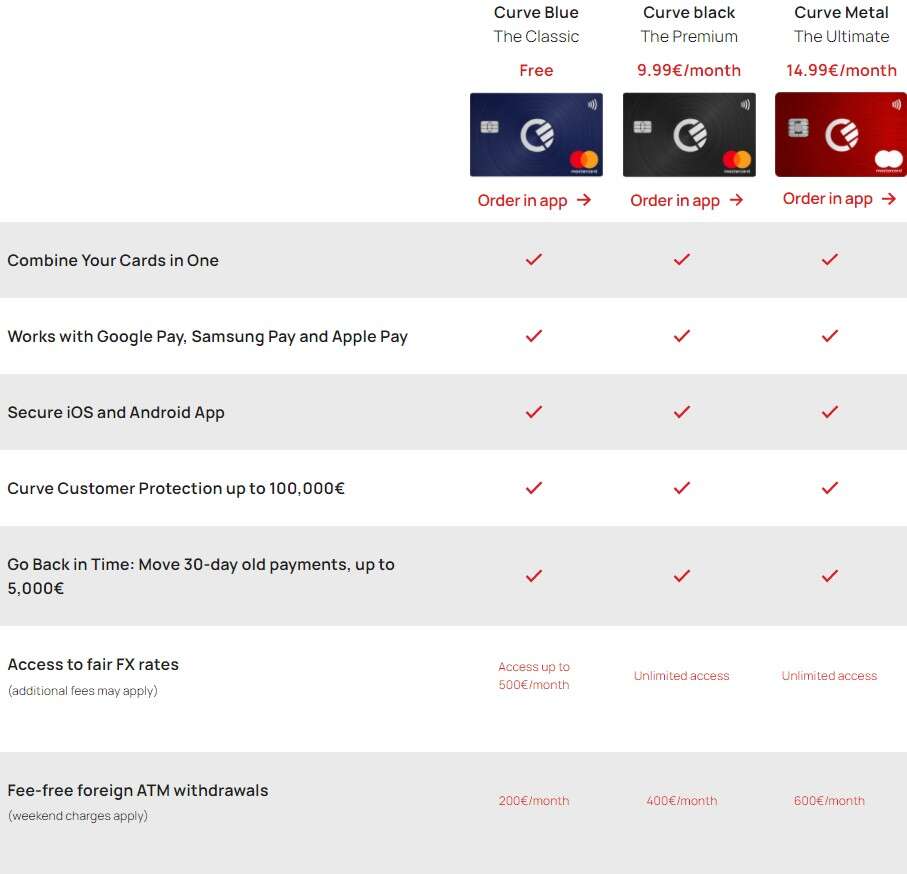

Fees

As visible in the image above, there is a fee-free limit for each tier and above that, the fees are a market conform 2%. For reference, my Beobank Credit cards charge 2.10%.

Upgrading the card is needed if you want to use the perks such as lounge access to increase your limits and thus have a lower chance of paying fees or enjoying their travel and mobile insurances.

A deeper look at Curve’s main selling points

The Curve card has multiple selling points:

- Linking cards

- Back in time

- Anti-embarrassment mode

- Cashback (unlimited as of the second tier) and Curve Cash

- Tracking expenses

- [OPTIONAL] (travel) insurances

Each feature in itself is not always as helpful, but you will see that combined, they make Curve the perfect card to use daily.

1. Linking your cards with Curve

Probably the most unique feature of Curve is that you can use this card as your only card and still pay for expenses with other cards because of the

linking. In practice, this truly is very useful at times, though not as much as Curve likes you to believe. The other features are arguably more useful, although it is linked to this feature.

2. Back in time

Paid on the wrong card? No biggie, just rewind. Switch payments from one card to another, up to 30 days after the payment was made of up to €5,000! Tap the transaction you want to move, click “Go Back in Time”, and swipe to the card you’d like to pay with instead. You just traveled back in time with your MasterCard!

3. Anti-embarrassment mode

Arguably the best feature with Curve is that if you have a VISA/MasterCard debit card -like a lot of crypto cards are- you don’t have to worry about having enough cash on your account. Curve will switch to your backup if that happens. You can then use the go back in time feature to still use your favorite crypto card to pay for the expenses you want to pay with them.

4. Cashback and Curve Cash

Curve cash is a virtual card in the Curve app. Your balance consists of money earned through cashback, promos, or referrals and any money sent to you from other people on Curve.

On rare occasions, Curve cannot process a refund to your bank account; it’ll land here where you can then spend it.

Cashback with Curve is possible in your first month of using the free card. You earn 1% cash back for your first 30 days. If you go premium, the cashback rewards are even better. Curve Black customers also get 1% cashback on three selected retailers for an unlimited time. And for Curve Metal customers, that doubles to 1% cashback on six retailers.

On top of that, Curve offers regular one-off cashback offers of up to 20% from brands like Amazon Fresh, Just Eat, Under Armour, Booking.com, and many more.

5. Tracking expenses

Less talked about but just as helpful, seeing all of the expenses you made with the different cards you have linked. You have two tabs:

- Timeline

- Insights

Curve timeline will show you what you’ve spent, when you’ve spent it, and where you’ve spent it. You’ll get (optional) notifications every time you spend.

Insights gives you a breakdown overview per card and per category of your spending across all your cards on Curve.

6. (Travel) insurances

Insurances only apply to the paid tiers. At first glance, it looks enticing, “free” insurance by AXA, but it isn’t of course. You pay €9.99 or €14.99/month for it. Sure, you get a higher ATM and FX limit as well as a select amount of cash back, but the main cost is their insurances.

For this extra fee, you do get quite a decent offering. Though if you look at the Insurance Product Information Document, simply put, the dumbed-down version of the Terms&Conditions, you will see a laundry list of exceptions. Add to that the first negative experiences with AXA, and you start to wonder if it’s worth it.

Is the Curve Debit MasterCard worth it?

If you have multiple credit or debit cards, then this is your card, as it effectively replaces a large part of your wallet.

On top of that, you get 1-month cash back welcome bonus on all your purchases, not just selected retailers.

The benefit of Higher-level cards depends on your spending and if you will use the added extras. Furthermore, depending on which retailers you select and how frequently you use them, you can get your monthly fee back faster or slower. Besides the monetary benefit, there are a number of other benefits and downsides to using it in Belgium.

Is Curve worth it in Belgium?

A big benefit for Europeans, and Belgians specifically -Eventhough credit cards aren’t that common- is that most (Belgian) banks are moving towards the Visa or MasterCard network. Thanks to this move, you can put cards like the HelloBank VISA debit card on Curve and use it as a backup for cards such as the Crypto.com Jade Green card.

Other reasons to (not) consider Curve are:

Conclusion

How do I summarize my experience with the Curve card?

While I haven’t used the card that long, I enjoy it every day thanks to it being free. The first month was exceptionally good thanks to the 1% cashback and the fee-free transactions costs while abroad. Because I have my crypto.com card that has unlimited free foreign transactions I use that instead of Curve if that limit is reached.

As I’m not sure how many times I’ll be abroad per year, I’m not getting the next tier just yet, though I might in the future. It will depend on the new limitations crypto.com will definitely put in place later this year. Travel insurance is moot for me as I have dedicated travel insurance plus insurance on my American Express Platinum card.

With that all said, All in all, I’m a satisfied Curve Debit MasterCard user and can recommend at least the free level to everyone.