Why Wall Street Can’t Model AI (And Why They’re Bungling MSFT and Adobe)

A few days ago, I dropped a comment on r/ValueInvesting about Microsoft (MSFT) and Adobe (ADBE), and the corresponding collective AI panic that was melting stock analysts’ brains. It seemed like I struck a chord, so I’m unpacking it in more detail here. The underlying point goes beyond just those three stocks.

The 95% Everyone Is Misinterpreting

In early 2026, AI stocks were repriced not on their fundamentals but on a single misread statistic. A few months back, a number spread like wildfire across financial media: 95% of corporate AI projects fail to deliver any measurable ROI. Tech journalists drooled over it. LinkedIn turned into an “I told you so” contest. Wall Street analysts used it as a blunt instrument to hammer the share prices of any company with “AI” in its pitch deck.

First off, the number exists, kinda. The interpretation is almost entirely wrong.

The stat comes from MIT Project NANDA’s State of AI in Business 2025 report (52 C-level interviews, 153 structured surveys, 300+ public deployments analyzed), so it is somewhat legitimate research. But the keyword in the finding is measurable. 95% of GenAI pilots showed zero measurable P&L impact. According to the researchers, the failure wasn’t the AI. It was messy corporate data, terrible workflow integration, and a total lack of internal tools to track whether the AI was actually doing anything.

MIT scientist Andrew McAfee made this point very clearly on De 7 Extra, the Belgian financial podcast by De Tijd. His take: companies are aggressively experimenting with AI, but they don’t have the dashboards to show a linear return on a quarterly spreadsheet yet. They’re flying without instruments. This breakdown goes into more detail on where the headline actually came from.

That is a radically different diagnosis from “AI doesn’t work.” Wall Street saw the headline and went with it cause of course, they did. SaaS and cloud companies got priced based on that overnight, as the entire tech thesis had just collapsed.

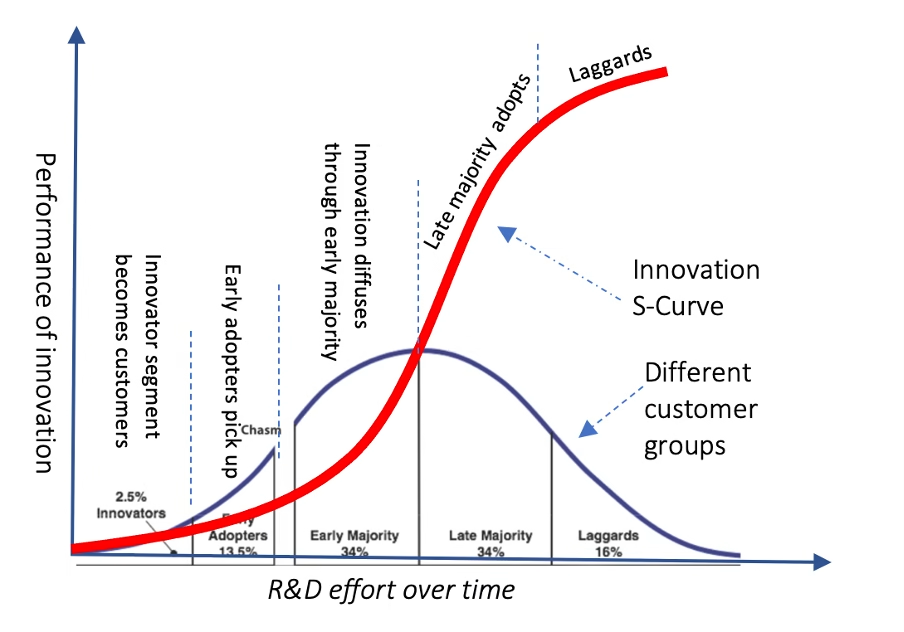

Treating an S-Curve Like a Quarterly Inventory Report

Here’s the thing. Technology adoption doesn’t move in a straight line. It follows an S-curve: a painfully slow start, a steep climb, and a final plateau. The internet, smartphones, and cloud computing all went through the exact same phase. Companies poured billions into infrastructure while the immediate, measurable return looked like pocket change. Then the curve went vertical.

Wall Street has a structural problem with this. Analysts work on 90-day reporting cycles. Their models are built for businesses with predictable, linear revenue relative to costs. When a company drops $190 billion into AI infrastructure over a few years, the spreadsheet panics -> Costs up -> Revenue unclear == Sell.

Wall Street has a structural problem with this. Analysts work on 90-day reporting cycles. Their models are built for businesses with predictable, linear revenue relative to costs. When a company drops $190 billion into AI infrastructure over a few years, the spreadsheet panics -> Costs up -> Revenue unclear == Sell.

The model can’t seem to look inside an enterprise workflow and see what’s actually changing. I can.

I work as a DevOps engineer. Every day I live inside Azure, EntraID, and Microsoft 365. I see AI integration happening in real time rather than in Press Releases. In the actual tools my team uses and builds on. We are slowly moving away from the experimentation phase in AI and agents, where we accepted no return, to a more critical view of usage and what we actually want to build for our customers.

This shift in usage just isn’t showing up on a quarterly P&L because nobody has figured out how to measure them yet. It’s what we are trying to figure out at this moment. This is exactly what MIT found.

When the people running the infrastructure tell you the technology is changing how work gets done, and a guy in a suit downgrades the stock because a 90-day capex report didn’t show an immediate linear return, I have a pretty good guess as to who is wrong.

Three AI Stocks Priced for Failure in 2026

Full disclosure: I’m long on all three. This is my own assessment, not financial advice.

1. Microsoft ($MSFT)

Azure grew 39% in constant currency in both Q2 and Q3 fiscal 2026, beating analyst estimates in both quarters. Microsoft’s AI business crossed a $37 billion annual revenue run rate in Q3, up 123% year over year. The stock is down roughly 35% from its all-time high because Wall Street looked at the capex plan climbing toward $190 billion and panicked. The narrative flipped from “AI monopolist” to “capex value trap” over the span of two earnings calls, compressing the P/E into the low-to-mid-20s. Punishing a stock for spending the exact capital required to generate 39% cloud growth and a $37 billion AI run rate is a strange kind of logic.

2. Adobe ($ADBE)

Adobe’s forward P/E has compressed to around 9x while the company is printing record revenues: $6.62 billion in Q2 fiscal 2026 (reported June 11, 2026), up 13% year over year, with strong free cash flow and a raised full-year guidance. AI-first ARR tripled year over year, surpassing $500 million. The bear case is that AI is eating Adobe’s moat overnight because Midjourney can make a pretty picture.

This completely misunderstands what Adobe is. Adobe isn’t a photography tool. It’s the creative workflow for every major brand, agency, and media company on the planet. Creative Cloud is embedded in professional pipelines in a way that a Midjourney subscription doesn’t replace. Adobe is also building its own AI (Firefly) directly into that same ecosystem. The valuation implies a catastrophic disruption that hasn’t materialised, while the financials show a business that won’t stop growing. I see this at my current client. They didn’t throw out Adobe at all, in fact, they are indeed looking to Firefly to streamline everything, hoping to save on the cost of tokens in the dedicated AI tools, as these costs are rising.

3. dLocal ($DLO)

This one is a bit of a wildcard. dLocal handles payments infrastructure in emerging markets (Africa, Latin America, South Asia), regions at the very beginning of their digital payment S-curves. Revenue in 2025 was up 46.6% year over year. The stock got hit hard during the broader SaaS and fintech sell-off on fears that AI implementation costs would wreck margins before paying off.

Analyst consensus targets are in the $17-18 range, well above where it trades now, with 8 Buy ratings and 0 Sell ratings. The irony? This isn’t even a pure AI play. dLocal uses AI for fraud detection and routing optimisation, but the core growth story is geographic expansion. It got caught in the AI panic purely by association.

The Analysts Are Just Guessing

Circling back to the MIT finding. If 95% of enterprises can’t measure their AI returns on a quarterly P&L, think about what that means for investors.

External analysts, the ones setting price targets and moving markets, are trying to model data that the companies themselves haven’t fully quantified yet. They have less information than management, who have less information than they need to tell a clean story to shareholders.

Confident modelling of “AI ROI” is mostly fiction right now. Analysts saying AI will kill Adobe’s moat next quarter are guessing. Analysts saying Microsoft’s capex is a bridge to nowhere are guessing. Journalists shouting about a 95% failure rate without reading the study are chasing clicks.

The market is treating a multi-year technology infrastructure cycle like a retail inventory problem. That creates situations in which high-quality compounding machines are discounted because a 90-day spreadsheet can’t capture a 5-year return. Whether MSFT, ADBE, and DLO are in those situations right now, nobody knows for certain.

The Part I Keep Coming Back To

I’ll end with what I wrote on Reddit, because I still haven’t found a better way to put it:

“When a high-quality compounding machine like Microsoft gets discounted to a low-20s P/E just because Wall Street lacks the patience to wait for capital investments to mature, that smells like an opportunity. But hey, I’m just a DevOps engineer working daily with Azure, EntraID, and MS365.”

The people best positioned to judge AI’s actual enterprise impact are the ones building the infrastructure. Not the guys tweaking rows in Excel.

What’s your take? Are AI stocks in 2026 being repriced on panic rather than fundamentals, or is the capex concern actually valid? And if you’re thinking about where passive investing fits alongside positions like these, I wrote about robo investing options in Belgium earlier this year. Drop your thoughts in the comments.

Positions disclosed: long MSFT, ADBE, DLO. None of this is financial advice.